There was a loud minority of analysts pondering we had been in, or imminently in, recession (see an inventory right here). It’ll be fascinating to see how these views are revised. Nevertheless, as I famous, whereas the information was not supportive of being in a recession as of October, three potentialities may reconcile observations with such views: (1) the mannequin is incorrect, (2) the recession is right here, however we don’t comprehend it, or (3) the recession continues to be to come back.

For example, right here’s the probit mannequin predictions from an ordinary time period unfold plus brief charge 12-month forward mannequin, estimated each 1986M01-2023M10 (so assumes no recession occurred as of October 2024) and 1986M01-2018M12 (the latter means it omits the 2020 pandemic recession).

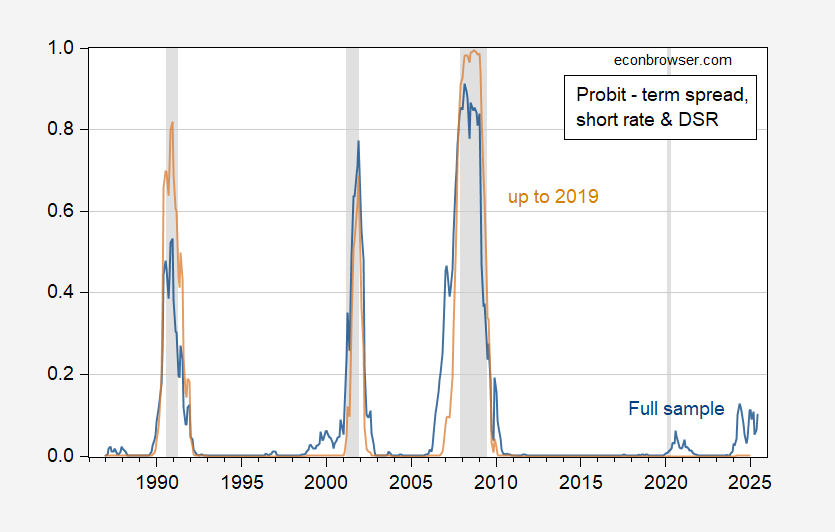

Determine 1: Estimated chance of recession 12 months forward utilizing 10yr-3mo time period unfold and 3mo charge, estimated over complete 1986-2023M10 pattern (blue), over restricted 1986-2018 pattern (tan). NBER peak-to-trough recession dates shaded grey. Supply: NBER and writer’s calculations.

Going by these estimated recession chances, the chance of being in a recession in January 2025 is 79% utilizing the complete pattern. Utilizing a pre-pandemic pattern, it’s 50%. Nevertheless, as famous in Chinn and Ferrara (2024), this easy specification is dominated when it comes to pseuo-R2 and AUROCs by specs together with international time period spreads and debt-service ratios. Augmenting the time period unfold & brief charge specification with debt service ratio (and utilizing real-time debt-service ratios) yields the next graph.

Determine 2: Estimated chance of recession 12 months forward utilizing 10yr-3mo time period unfold, 3mo charge, and debt-service ratio, estimated over complete 1986-2023M10 pattern (blue), over restricted 1986-2018 pattern utilizing related classic of debt-service ratio (tan). NBER peak-to-trough recession dates shaded grey. Supply: NBER and writer’s calculations.

The pseudo-R2 for the time period unfold plus brief charge is 0.21, whereas that for the debt-service augmented specification is 0.56 (full pattern estimates).

The pre-pandemic estimates point out zero chance of recession as much as December 2024, whereas a full pattern estimate yields 11% chance in January 2025. Including in a international time period unfold (a la Ahmed and Chinn (2024)) pushes up that chance to 23%.

If the proper mannequin is the DSR-augmented specification, then a recession within the subsequent yr isn’t foreseen by the markets. However, if one thing sudden happens between now and 12 months from now (e.g., pandemic, battle), then the end result is perhaps very totally different from the market’s expectation.

Addendum: 5pm CT

Or…one may see what the betting markets are saying about two consecutive quarters of detrimental GDP development in 2025 (presumably utilizing advance launch for the 2nd consecutive quarter…)

Supply: Kalshi, 9 Nov 24, 5pm CT.

Polymarket makes use of the NBER BCDC name as a payout criterion.

{kind=link}