Reader Michael writes:

…excessive revenue wage development has grown a lot quicker than medium and low revenue wage development patterns.

Right here’s a stab at having a look on the knowledge. First wages:

Determine 1: 12 months-on-12 months development fee in common hourly earnings from CES (blue), common wage from CPS (inexperienced), median wage from CPS (tan), from 2nd quintile (purple), all in %. NBER outlined peak-to-trough recession dates shaded grey. Supply: BLS, Philadelphia Fed Wage Tracker, NBER, and creator’s calculations.

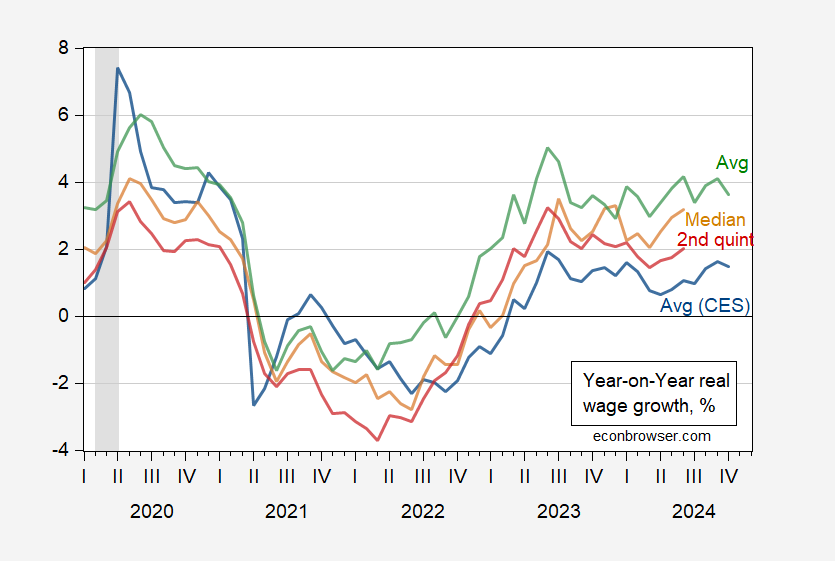

What about relative to inflation? Right here, one would attempt to match up with essentially the most applicable deflators. Right here’s my try.

Determine 2: 12 months-on-12 months development fee in common hourly earnings from CES, deflated by CPI-U (blue), common wage from CPS, deflated by CPI-wage earners (inexperienced), median wage from CPS, deflated by median family revenue CPI (tan), from 2nd quintile deflated by 2nd quintile family revenue CPI (purple), all in %. NBER outlined peak-to-trough recession dates shaded grey. Supply: BLS, Philadelphia Fed Wage Tracker, BLS, NBER, and creator’s calculations.

So year-on-year actual wage development has been optimistic from between 2022M10 to 2023M02 onward.

{kind=link}