Mark Sobel at OMFIF discusses the probability of an new Plaza Accord to depreciate the greenback. Given one would want Euro space and Chinese language settlement, the assessed chances are low

A Mar-a-Lago Accord additionally can be inconsistent with Europe’s cyclical scenario. A devalued greenback can be tantamount to a stronger euro. That could possibly be achieved by greater ECB rates of interest and/or fiscal enlargement in key European nations. However the ECB is now slicing charges given weak European economies and key nations akin to Italy and France lack fiscal house.

G3 overseas trade market jawboning and interventions, absent adjustments in fundamentals, are largely ineffective. In fact, trade charges are pushed by the whole steadiness of funds, usually reflecting rate of interest differentials, and thus it’s nearly unattainable to foresee how capital flows and trade charges would possibly reply to any accord.

Would China conform to an accord?

Trump’s ‘devaluation’ rhetoric is closely geared toward China. China was not a celebration to the Plaza Accord however it will should be central to a Mar-a-Lago Accord.

…

A weakening renminbi poses conundrums for Chinese language authorities. The renminbi is already falling towards the greenback, in the direction of 7.3 at present, reflecting in massive measure common greenback power and anticipation of tariffs (Determine 1). However sharp depreciation towards the greenback runs the danger of spawning an enormous one-way capital outflow as occurred in 2015-16, an expertise China doesn’t wish to see replicated. The authorities may need some temptation, nevertheless, to let the renminbi fall in a restrained method to offset the impression of tariffs and ship Trump a message.

This text spurred me to look at the US efficient trade price, measured utilizing (the conventionally used) CPI and unit labor prices (the latter extra related for evaluating “competitiveness” — see dialogue right here).

Determine 1: CPI deflated commerce weighted worth of US greenback (blue), and ULC deflated worth of US greenback(tan), each in logs 2000Q1=0. NBER outlined peak-to-trough recession dates shaded grey. CPI sequence is Fed items commerce weighted sequence spliced to items and providers commerce weighted sequence at 2006M01. 2024Q4 statement is for October-November. Supply: Federal Reserve Board, and OECD, each through FRED, NBER, and creator’s calculations.

So on each CPI deflated and ULC deflated (“competitiveness”) phrases, the greenback is certainly not as sturdy because it was within the mid-1980’s. So why the Trumpian fixation on the trade price? Are trade charges inessential to the commerce steadiness? I’d say no, having been the contributor to many papers on the elasticities method to commerce flows (see right here and right here). Nevertheless, I’d additionally say that on the medium run, personal saving relative to funding, and public saving (i.e., the funds steadiness) are going to be key determinants of the present account and not directly then the commerce steadiness (as within the IMF’s earlier Macroeconomic Steadiness method underlying CGER, and Chinn and Prasad (2003), and varied Chinn-Ito papers [1] [2] [3] [4]).

The Trumpian thought of forcing a depreciation of the greenback will then seemingly have little medium time period impact on the commerce steadiness within the absence of in some way adjusting macroeconomic balances (admittedly, throwing the US economic system right into a recession would tank funding, (S-I) would improve and ceteris paribus the present account enhance).

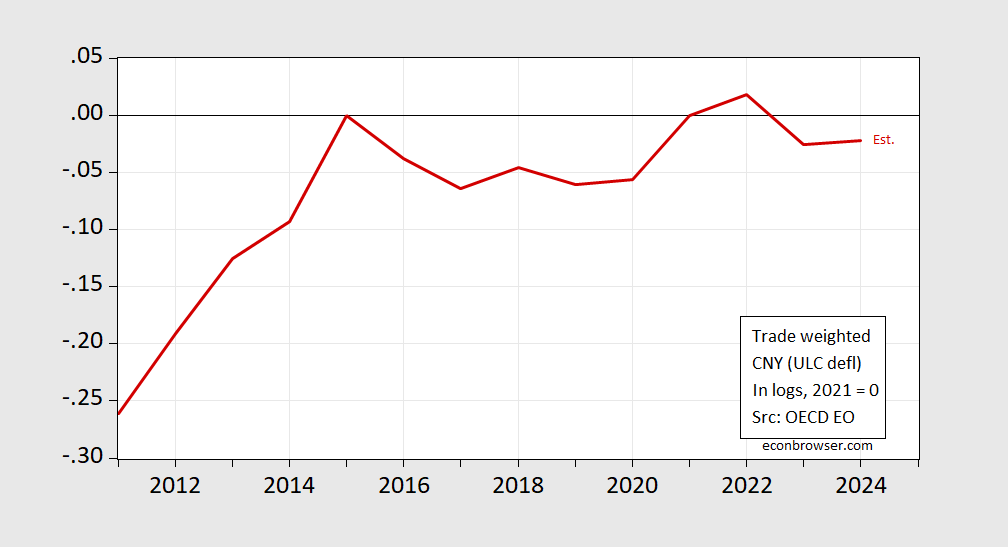

On the purpose that China is unlikely to let it’s forex recognize towards the US greenback, it’s attention-grabbing to examine not solely the CPI deflated yuan (as Sobel does), but additionally the ULC deflated yuan (this took some searching round):

Determine 2: ULC deflated worth of Chinese language yuan (crimson), in logs 2021=0. ULC is economywide. 2024 statement is forecast. Supply: OECD, Financial Outlook statistical appendix, December 2024.

The Chinese language are attempting to spur development of their economic system, partly by spurring web exports. Appreciation works towards this.

By the way in which, if certainly the Trump administration plans to slap a 60% tariff on China, simply keep in mind the usual deviation of the month-on-month change within the CNY/USD trade price (2018-2024) has been about 1.3% (not annualized). On the attainable value of capital flight, the Chinese language may permit substantial yuan depreciation, though as Sobel notes, a extra “managed” depreciation may be applied.

At a minimal, don’t count on a grand plan to rearrange euro and yuan appreciation.

{kind=link}