JW Mason asserts that, in specializing in the true alternate charge, I’m on the facet of relative costs being the first determinant of flows.

Right here is among the huge cleavages between orthodox and (Put up) Keynesian approaches to worldwide economics: are commerce flows primarily pushed by relative costs, or by demand?

Quite the opposite, I feel incomes are crucial. That is demonstrated by my work on commerce flows defined right here. Updating, to 2024, I estimate for 1980-2024:

Δ exp t = β 0 + φ exp t-1 + β 1 y *t-1 + β 2 q t-1 + γ 1 Δ y *t + γ 2 Δq t + u t

Δ imp t = β 0 + φ imp t-1 + β 1 y t-1 + β 2 q t-1 + γ 1 Δy t + γ 2 Δq t + seven lags of Δq t + u t

Every error correction mannequin specification features a covid dummy (2020Q1-Q2) and first distinction thereof.

For US exports of products and providers:

This suggests the long term elasticity of exports with respect to the greenback alternate charge is 2.07, whereas that of revenue (rest-of-world trade-weighted GDP) is 1.47.

This compares with a 2.3 and 1.9 as present in Chinn (2004).

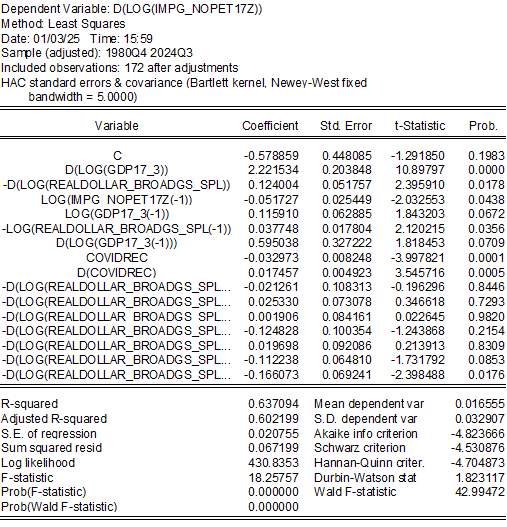

For items imports, the true alternate charge is vital as nicely, though it’s tougher to acquire a statistically important estimates.

The lengthy lags within the alternate charge are per quite a few research indicating that the consequences of the alternate charge take a very long time to have an impact (it’s per the graph on this put up).

The long term elasticity of products imports (ex-oil) with respect to the greenback is 0.74, and with respect to US revenue is 2.24.

In Chinn (2004), I receive long term estimates of -0.2 and a pair of.3 for complete imports, respectively. In Chinn (2010), I receive estimates of -0.5 and a pair of.2 respectively, for ex-petroleum items imports, for knowledge as much as 2010.

Therefore, revenue is vital, as are relative costs. I consider this as a standard view (see e.g., Rose and Yellen, JME 1989), reasonably than orthodox vs. post-Keynesian view.

Now, as for relative significance, one can take a look at standardized (or “beta”) coefficients, that are OLS coefficients divided and multiplied customary deviations. For an exports regression estimated in first variations, the revenue “beta” coefficient is about 4 occasions the dimensions of that for the alternate charge. For the non-oil items import first variations equation, the revenue “beta” coefficient is about ten occasions that of the alternate charge coefficient.

{kind=link}