CNN printed an article immediately, entitled “What’s actually taking place in America’s financial system”. Most factors are standard, however one graph was attention-grabbing – bank card debt:

Supply: CNN.

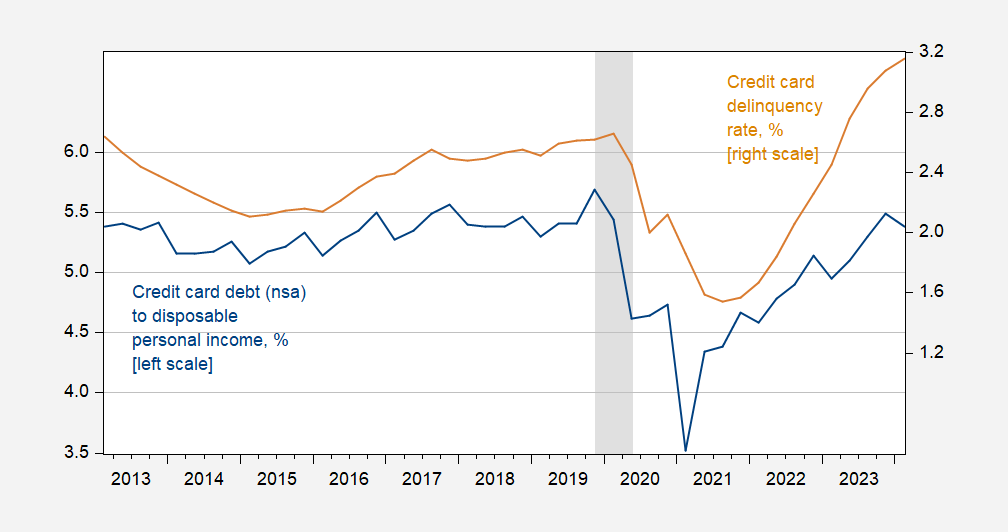

Apart from the standard complaints that this quantity was not normalized by disposable private earnings, or GDP, this struck me as a humorous indicator to glom onto. Right here’s normalized bank card debt together with delinquency fee.

Determine 1: Bank card debt (n.s.a.) to disposable private earnings, % (blue, left scale), and bank card delinquency fee for all industrial banks, % (tan, proper scale). NBER outlined peak-to-trough recession dates shaded grey. Supply: NY Fed; Federal Reserve Board and BEA by way of FRED, NBER, and creator’s calculations.

So bank card debt normalized goes down in Q2, however delinquencies are rising. This means that one thing is happening, for some segments of the inhabitants, even whereas family debt-to-GDP and family debt service to disposable earnings ratios are falling.

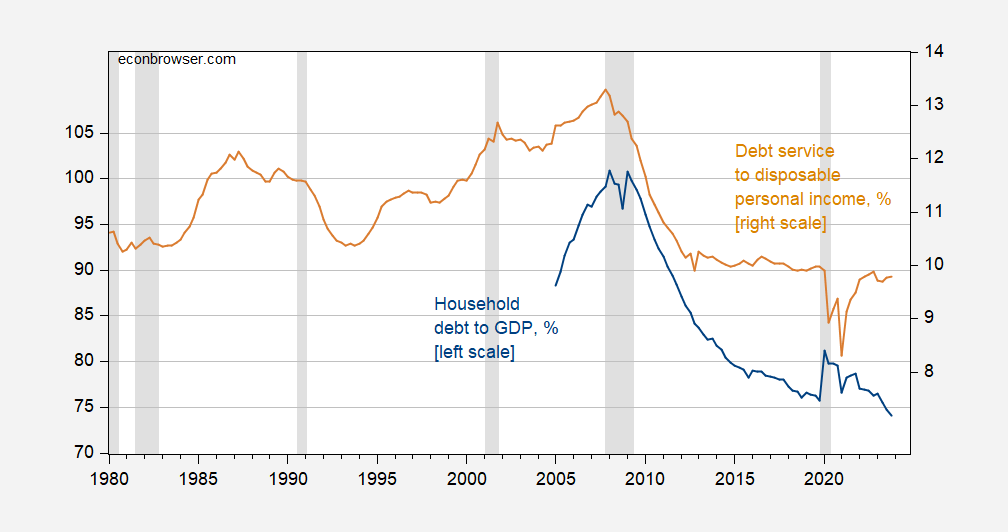

Determine 2: Family debt to GDP, % (blue, left scale), and debt service to disposable earnings fee, % (tan, proper scale). NBER outlined peak-to-trough recession dates shaded grey. Supply: IMF by way of FRED, Federal Reserve Board by way of FRED, NBER.

Debt service could be fixed at the same time as rates of interest rise as a result of pervasiveness of mounted fee mortgages. So, credit score woes are doubtless extra urgent for some earnings segments than others.

{kind=link}