The summary from article forthcoming within the Journal of Worldwide Cash and Finance.

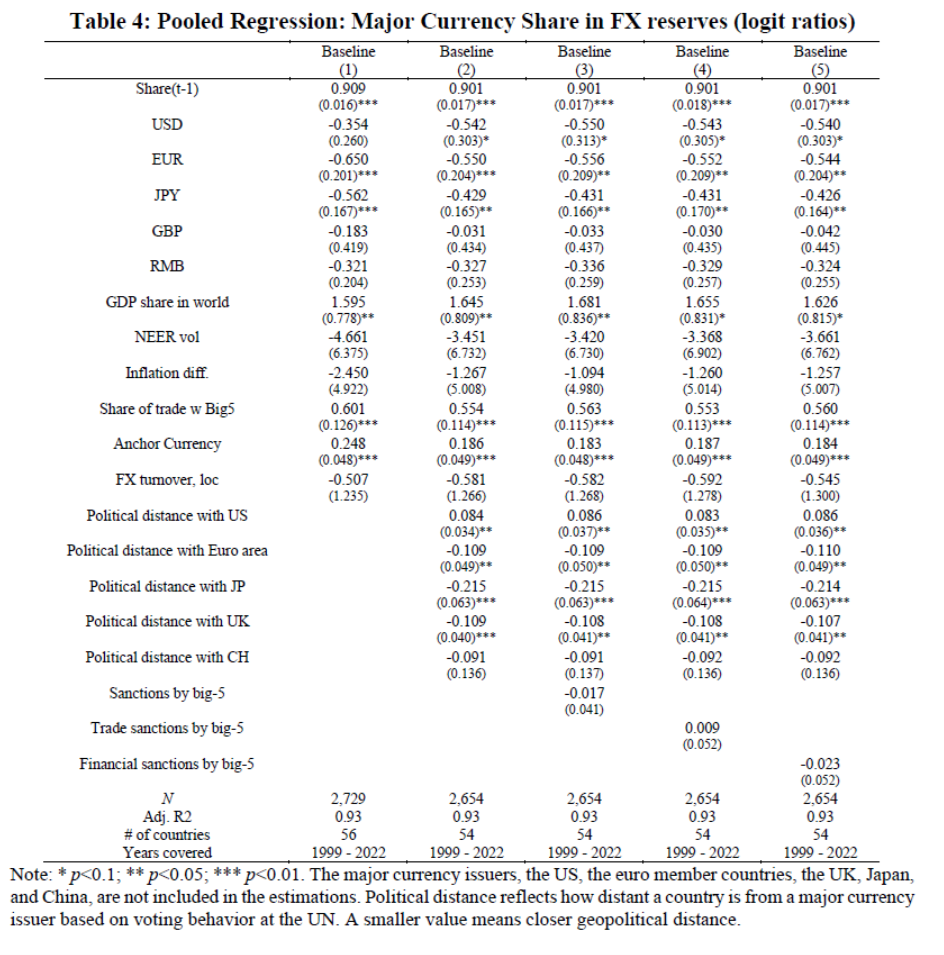

We start by analyzing determinants of mixture overseas change reserve holdings by central banks (measurement of issuing nation’s financial system and monetary markets, capacity of the forex to carry worth, and inertia). However understanding the willpower of reserve holdings most likely requires going past the mixture numbers, as a substitute observing particular person central financial institution conduct, together with traits of the holding nation (bilateral commerce with the issuing nation, bilateral forex peg, and proxies for bilateral publicity to sanctions), along with the traits of the reserve forex issuer. On a currency-by-currency foundation, US greenback holdings are considerably nicely defined by a number of issuer traits; however the different currencies are much less efficiently defined. It might be that the outcomes from currency-by-currency estimation are impaired by inadequate pattern measurement. This consideration affords a motivation for pooling the information throughout the most important currencies and imposing the constraints that reserve holdings are decided in the identical manner for every forex. On this setting, most financial determinants enter with significance: financial measurement as measured by GDP, bilateral forex peg, and bilateral commerce share. Whereas one geopolitical issue (congruence in voting within the UN) is usually vital within the anticipated method (excluding the US greenback), the opposite geopolitical issue (sanctions) doesn’t enter with significance.

Right here’s an image of the mixture forex shares, from the IMF’s COFER database, up to date knowledge launched on June eleventh.

Determine 1: Share of overseas change reserves held by central banks, in USD (blue), EUR (orange), DEM (tan squares), JPY (inexperienced), GBP (sky blue), Swiss francs (purple), CNY (pink). For 1999 knowledge onward, estimates primarily based on COFER knowledge, and apportionment of unallocated reserves, described in textual content. Supply: Chinn and Frankel (2007), IMF COFER accessed 6/20/2024, and creator’s estimates.

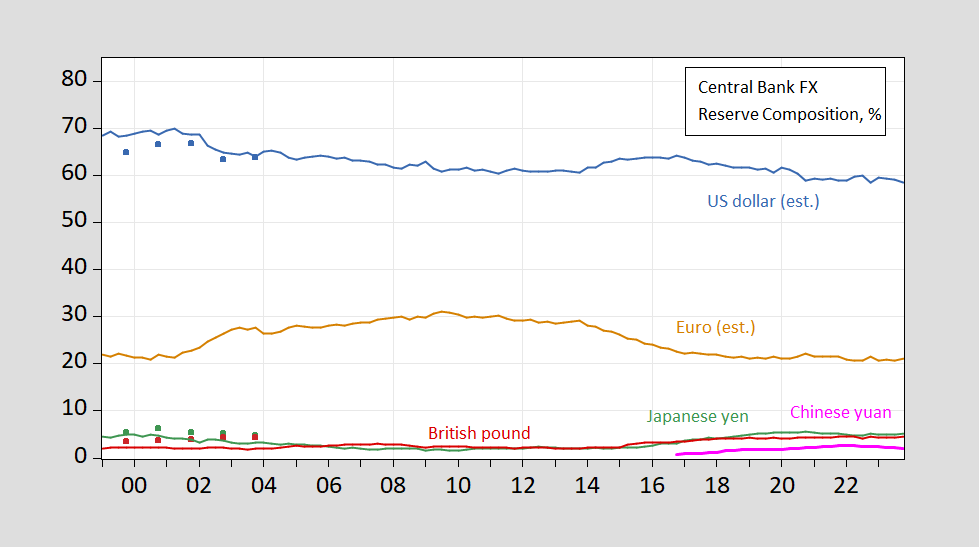

And right here’s a element, for 1999 onward:

Determine 2: Share of overseas change reserves held by central banks, in USD (blue), EUR (orange), JPY (inexperienced), GBP (sky blue), Swiss francs (purple), CNY (pink). For 1999 knowledge onward, estimates primarily based on COFER knowledge, and apportionment of unallocated reserves, described in textual content. Supply: Chinn and Frankel (2007), IMF COFER accessed 6/20/2024, and creator’s estimates.

Equations used to estimate mixture shares pre-EMU are fairly ineffective in predicting shares now. Therefore, on this new paper, we depend on particular person central financial institution knowledge to estimate the determinants of shares. The outcomes of a pooled cross-country cross-currency, unconstraining the geopolitical distance coefficient to fluctuate throughout forex, are reported in Desk 4.

Supply: Chinn, Frankel, Ito (forthcoming, JIMF).

Following the ends in Chinn and Frankel (2007), we discover financial measurement issues, in addition to inertia. Whereas we discover retailer of worth measures (inflation, change price volatility) have a detrimental affect, these results will not be statistically vital. This particular knowledge set (central financial institution by 12 months) permits us to research the affect of commerce flows and peg, which seems to be necessary. We replicate the discovering obtained by Goldberg and Hannaoui (2024) that extra geopolitically distant international locations (as measured by coincidence in UN GA voting) maintain better greenback shares, whereas the reverse is true for the opposite currencies. Whereas monetary sanctions have a detrimental affect, the measured sensitivity isn’t statistically vital.

Whereas we don’t explicitly report how greenback shares have declined, it’s helpful to notice that different research (see Arslanalp, Eichengreen and Simpson-Bell (2024), and references therein) have documented that the slack isn’t usually being largely take up by the RMB, however different unconventional currencies.

See additionally Eswar Prasad’s current International Affairs piece, the Third annual Fed-FRBNY convention on the worldwide roles of the greenback, Kamin and Sobel (2024), Atlantic Council “Greenback Dominance Monitor”.

{kind=link}