CBO projection and SPF imply forecast diverge, by practically a share level in 2024.

Determine 1: Ten 12 months Treasury yield (black), projected by CBO (tan), SPF imply (blue), TIPS ten 12 months (crimson), all in %. NBER peak-to-trough recession dates shaded grey. Supply: Treasury by way of FRED, CBO, Philadelphia Fed, NBER.

CBO’s projection relies on present regulation, whereas the varied forecasters within the SPF are usually not equally constrained. That, I believe doesn’t clarify the distinction.

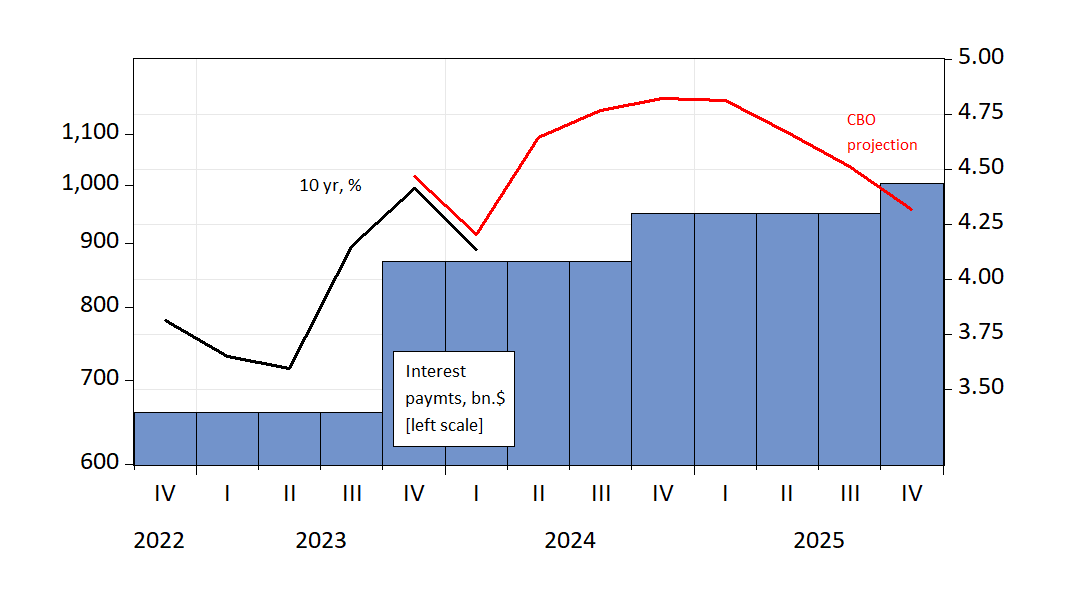

The implications for curiosity funds (therefore complete vs. major deficit) differ as a consequence.

Determine 2: Federal curiosity funds in bn.$, SAAR (blue bar, left log scale), and ten 12 months Treasury (black), and CBO projection (crimson), each in % (proper scale). 2024Q1 is for January-February. Supply: CBO, Treasury by way of FRED.

{kind=link}