At present we current a visitor publish written by Lindsay Jacobs, Assistant Professor on the Robert M. La Follette Faculty of Public Affairs, on the College of Wisconsin, Madison.

Since 2021, Social Safety retirement advantages have exceeded the income generated by payroll taxes. The shortfall has been coated by drawing from the Social Safety Belief Fund, which is projected to be depleted by 2034. At the moment, we’ll face a “fiscal cliff” for this self-funded program the place payroll taxes will solely cowl about 80% of the advantages, leading to an automated 20% discount in funds to retirees.

Almost all employees and retirees will probably be affected, so there may be broad curiosity in reforms that may avert this sudden drop in advantages. Nevertheless, this final result is sooner or later, so the dilemma is that whereas any reform is best than inaction, every comes with instant prices. Contemplating this, the restricted legislative momentum appears unsurprising.

The Social Safety Administration (SSA) has revealed up to date projections displaying how numerous reforms might influence this system’s solvency. Yow will discover a abstract right here, and extra detailed analyses right here. There are dozens of prospects, most being variations on both profit discount or payroll tax will increase. Two steadily mentioned reforms are elevating the retirement age and elevating or eliminating the payroll tax cap. Different, much less outstanding proposals contain adjusting how advantages and earnings histories are calculated to account for inflation and actual wage development.

In my opinion, profitable reform will doubtless contain a mixture of approaches with a purpose to preserve this system’s goal of poverty discount in outdated age whereas preserving the broad public help that Social Safety has loved.

Right here’s how I’m fascinated with the tradeoffs of 4 specific reform prospects—not as a policymaker however merely as an researcher. It’s extra of a novel than I had anticipated, but it surely turns on the market’s quite a bit to contemplate!

Reform 1: Elevating the Full Retirement Age

The Full Retirement Age (FRA)—the age at which beneficiaries can obtain their full Main Insurance coverage Quantity (PIA)—was regularly raised from 65 to 67 following important reforms in 1983. Surprisingly, these have been the final main adjustments to this system. Since then, proposals have surfaced to regularly increase the FRA additional to 68, 69, and even 70, with the rationale being that will increase in life expectancy justify a later retirement age.

This transformation can be fairly efficient in enhancing Social Safety’s solvency. For instance, elevating the FRA regularly to age 69 would scale back this system’s shortfall by about 38% over the following 75 years. (Situation C1.4 in SSA’s projections.)

I’d argue that there are further distributional results of accelerating the FRA throughout occupations, given the variations in claiming age conduct and there being a good larger penalty on teams of people that have a tendency to assert early. Specifically, individuals in blue-collar jobs, no matter their revenue stage, are likely to retire earlier and can be extra negatively impacted by an FRA improve. I mentioned this in a previous EconBrowser article and this paper additional explores the problem.

Elevating the FRA isn’t an particularly standard reform. Whereas it’s successfully a profit reduce, as proven beneath, it doesn’t require delaying advantages altogether; the choice to assert advantages earlier than the FRA—on the Early Eligibility Age (EEA) of 62—would nonetheless stay, albeit at lowered ranges. If this level have been emphasised, I believe the concept would possibly face much less resistance.

A rise within the earliest eligibility age can be a far worse final result for many who are already claiming as quickly as attainable—notably many blue-collar employees. Elevating the EEA would doubtless even have the impact of directing extra individuals towards making use of for Social Safety Incapacity Insurance coverage (SSDI).

I wouldn’t be in favor of accelerating the FRA dramatically or the EEA in any respect as a result of they make advantages far much less progressive in apply, and fewer in keeping with the aim of this system. A average improve within the FRA to 68 appears agreeable, at the least when contemplating the choice of across-the-board profit cuts that may include insolvency.

Reform 2: Growing the Taxable Wage Base

The wage base for Social Safety payroll taxes contains all revenue as much as the present annual most of $168,600, and is taxed at 12.4%, break up between employers and staff. Any revenue above this cover isn’t topic to the tax, and no further advantages are earned. At present, about 6% of employees earn greater than this threshold. Whereas advantages are extremely progressive, payroll taxes alone are considerably regressive.

One of many extra formidable proposals to develop the wage base is to carry the cap solely, taxing all revenue whereas sustaining the present profit components. This might remove about 60% of the projected funding shortfall over the following 75 years (as proven in Situation E2.17 in SSA’s projections). A variation of this proposal was included within the Social Safety 2100 Act (H.R. 4583), which might topic revenue above $400,000 to the payroll tax, whereas excluding revenue between $168,600 and $400,000. This creates a “donut gap” that may shrink over time because the taxable most will increase with wage development.

Eliminating the payroll tax cap altogether would definitely strengthen the Social Safety program financially however would include many downsides. An actual concern can be the unknown however doubtless very giant labor market results; excessive earners and their employers would certainly search methods to restructure compensation to keep away from the tax. Even when one have been sympathetic to greater tax charges for greater earners, is Social Safety solvency the very best precedence use of these revenues?

One other subject is the attainable decline in help for this system. This system is at present very fashionable, partially as a result of advantages are broadly seen as honest—extremely progressive, however nonetheless linked to taxes paid. Eradicating the cap would weaken the connection between contributions and advantages, which can erode help amongst greater earners. Even when further profit credit have been supplied to these paying greater taxes, this wouldn’t be very interesting to wealthier people who produce other most well-liked financial savings choices.

One option to mitigate a few of these issues is perhaps to impose a decrease tax charge on revenue above the present cap, which might soften the influence on excessive earners and make the reform extra palatable.

There’s a convincing argument for increasing the taxable wage base, however such a reform would doubtless must be tempered. At the moment, 83% of complete labor earnings are topic to Social Safety taxes, down from over 90% within the years following the 1983 reforms. Though the taxable most adjusts for wage inflation, revenue inequality has grown, that means a larger share of earnings now exceeds the cap. A reform that would handle this subject can be to boost the utmost revenue taxed to cowl 90% of taxes, as a substitute of indexing to development in common wages. This is able to put the cap at about $300,000 at present. argument towards doing so is that what has pulled up the typical earnings isn’t a lot the highest 10% of earnings however reasonably the share on the very high.

Reform 3: Decreasing the Actual Progress of Advantages

One delicate however extremely efficient reform would contain adjusting Social Safety advantages utilizing adjustments in general value ranges as a substitute of wage ranges to calculate previous earnings and corresponding advantages. Whereas common wages have outpaced inflation—reflecting actual productiveness development and leading to advantages that develop sooner than the price of dwelling—this reform would gradual that development. In keeping with the SSA’s projections (Reform B1.1 of their projections), this transformation alone might remove 85% of the Social Safety shortfall over the following 75 years.

To see why this may have such a big impact, it helps to consider how advantages are calculated. Advantages are based mostly on an individual’s delivery yr, the age at which they declare, and their high 35 years of earnings. These previous earnings are adjusted for wage inflation to find out an individual’s Common Listed Month-to-month Earnings (AIME), which is then used to calculate their Main Insurance coverage Quantity (PIA)—the month-to-month profit they’d obtain at Full Retirement Age (FRA). Changes are made if somebody claims earlier or later than their FRA. As a result of nominal wage development is sort of all the time greater than value inflation as a consequence of rising actual productiveness, the cumulative results of transitioning to cost inflation-based changes would considerably gradual the expansion of advantages over time. Whereas we’d all favor extra salient reforms, the complexity of this reform would possibly—nevertheless unlucky—truly make it extra politically possible.

The conceptual argument for this reform is that the present wage-level changes to advantages are extreme, rising retirees’ advantages effectively past buying energy.

An argument towards it’s that as productiveness rises, retirees ought to share within the positive factors from rising dwelling requirements by way of advantages linked to wage development. In spite of everything, if individuals might have as a substitute invested what they paid in Social Safety taxes through the years, their returns can be greater than inflation.

I’m keen on each traces of reasoning. Nevertheless, I believe the first benefit of this reform is that it’s merely very efficient at enhancing solvency whereas additionally disbursing prices over time.

Reform 4: Modifying the PIA Components to Cut back Advantages for Increased Earners

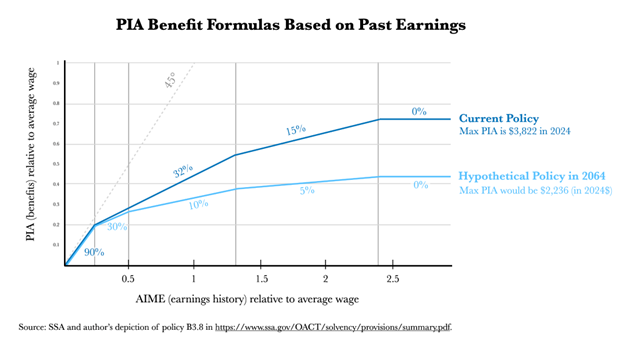

One other potential reform is to switch the Main Insurance coverage Quantity (PIA) components in a method that reduces advantages for all however the lowest earners. This is able to defend lower-income retirees from across-the-board profit reductions, whether or not these outcome from elevating the Full Retirement Age (FRA), altering how previous earnings are calculated, or any variety of different reforms. It might additionally considerably enhance Social Safety’s solvency.

To see what this appears like, I graphed the present PIA “bend factors” and elements, alongside the reform projection in B3.8, which might regularly alter the PIA components over 4 a long time and remove 29% of this system’s shortfall over the following 75 years.

This is able to make this system much more progressive, which might understandably cut back help because it weakens the hyperlink between the taxes individuals pay and what they’ll count on to obtain.

Regardless of this, it appears cheap on the grounds that it will go a good distance in enhancing solvency, whereas aligning extra intently with this system’s authentic goal of lowering poverty at older ages.

Furthermore, implementing the adjustments over an extended time horizon would give those that are able to saving to regulate their plans effectively prematurely of retirement—very fascinating when contemplating the choice of sudden and unsure drops in advantages.

Selecting the Least Worst Choices

In the end, I believe the objectives of Social Safety reforms ought to embody:

- Reaching solvency to satisfy present obligations and supply certainty for future retirees.

- Guaranteeing revenue substitute and safety towards poverty in outdated age, in alignment with this system’s authentic objectives.

- Preserving the broad help Social Safety has historically loved.

Given these targets—and contemplating the fact that the choice isn’t any reform, which is able to result in sudden profit cuts—I’d advocate for a mix of the next: lowering advantages for prime earners over time (Reform 4), adjusting how previous earnings are listed (Reform 3), and reasonably rising the taxable wage base (Reform 2). Taken collectively, a extra tempered model of every could possibly be carried out to attain solvency.

Of those, the best in reaching these objectives would doubtless be lowering advantages for greater earners (Reform 4), carried out regularly. Some type of this may align Social Safety extra intently with its authentic intention as a “security internet” aimed toward stopping poverty in outdated age, reasonably than a full retirement financial savings program. As a result of individuals with greater earnings histories have a tendency to save lots of way more privately, a discount in advantages is perhaps most well-liked to payroll tax will increase that may in any other case come up.

A average improve within the taxable wage base, masking nearer to 90% of complete earnings, contributes very successfully to this system’s instant solvency. Since adjustments to the profit components would take time to part in, at the least some near-term tax will increase are essential. Adjusting how previous earnings are listed—transferring towards a measure between wage and value inflation—would additionally assist obtain solvency whereas being extra impartial than different types of profit reductions.

With these choices accessible, I wouldn’t favor elevating the Full Retirement Age (Reform 1), because it disproportionately impacts those that for numerous causes declare earlier, notably these in bodily demanding jobs, and would doubtless improve reliance on Incapacity Insurance coverage (SSDI), which I’ve checked out right here.

The final important reforms in 1977 and 1983 occurred inside a yr of insolvency—so is that what we must always count on? Maybe, however the sooner reforms come, the higher. For legislators, nevertheless, advancing disagreeable however essential reforms are a principally thankless job with many downsides. This might change if a large share of voters present concern. However this may require accepting the fact of no reform: Our present coverage is an instantaneous discount of 20% in advantages for all in solely 10 years, a discount that may solely develop over time. With out this unlucky various in thoughts, in fact no reform appears interesting!

So, what do you assume?

This publish written by Lindsay Jacobs.

{kind=link}