Right this moment, we’re lucky to have Willem Thorbecke, Senior Fellow at Japan’s Analysis Institute of Economic system, Commerce and Business (RIETI) as a visitor contributor. The views expressed symbolize these of the creator himself, and don’t essentially symbolize these of RIETI, or another establishments the creator is affiliated with.

China’s merchandise exports elevated from $62 billion in 1990 to $3.6 trillion in 2022. In 1990, China’s exports equaled 1.9% of world exports and in 2022 its exports equaled 14.3% of world exports. China’s export juggernaut threatens corporations and jobs in importing nations. How does the renminbi have an effect on China’s exports?

Cheung et al. (2012) examined how Chinese language combination exports deflated utilizing the Hong Kong re-export unit worth index responded to the IMF CPI-deflated actual efficient alternate charge and to export-weighted actual GDP over the 1994-2010 interval. Using dynamic strange least squares (DOLS) estimation, they reported alternate charge elasticities which might be accurately signed and statistically vital. These point out that if the renminbi had been 10% weaker, the regular state degree of exports can be between 9% and 16% larger.

How Change Charges Might Have an effect on China’s Exports Now

Change charges could not have an effect on China’s exports lately as they did throughout the interval that Cheung et al. (2012) investigated. China’s export basket now contains many extra superior merchandise similar to equipment, electronics, chemical substances, and automobiles than it did over the pattern interval that Cheung et al. investigated. As extra subtle items are tougher to supply than easy items, it’s tougher to seek out substitutes for these items than it’s for ubiquitous merchandise. Since discovering substitutes is tougher, worth elasticities ought to be decrease for advanced items.

As well as, Jean et al. (2023) discovered that China in 2019 possessed a share of greater than 50% of worldwide exports in 600 merchandise. This was six instances higher than the U.S. or Japan and greater than twice as a lot because the European Union taken as an entire. They famous that when Chinese language exporters have a dominant market share in a product, it’s tough for importers to seek out substitutes. This might trigger the worth elasticity of demand for items the place China is dominant to be decrease.

However, extra of the value-added of the merchandise that China now exports comes from China. Xing (2021) documented the rise of Chinese language manufacturers producing cellphones. Branded corporations obtain extra of the return from items they produce than contract producers do. As well as, McMorrow (2024) confirmed that a lot of the value-added going into Huawei’s laptops now comes from China. Ahmed et al. (2016) and de Soyres et al. (2021) introduced proof indicating that the impression of alternate charges on exports will increase as extra of the value-added of the product is produced inside a rustic.

Time Sequence Proof on China’s Export Elasticities

It’s thus an empirical query whether or not alternate charges have a higher impression on China’s exports lately than they did in earlier years. Chen Chen, Nimesh Salike, and I are investigating this query. First we use DOLS estimation and quarterly information on China’s actual exports to the world over the 1994Q4-2023Q3 pattern interval. The dependent variables embrace the Financial institution for Worldwide Settlements CPI-deflated actual efficient alternate charge and actual GDP in OECD nations. Minimizing Dickey-Fuller t-statistics and inspecting Dickey-Fuller autoregressive statistics level to a break within the export collection throughout the World Monetary Disaster. A dummy variable is about equal to 1 starting in 2009Q2. The dummy variable can also be interacted with a development time period and with the alternate charge.

The outcomes are introduced in Desk 1. Column (2) permits for a differential development and for a change within the alternate charge elasticity starting in 2009Q2. The coefficients on the actual efficient alternate charge and the actual efficient alternate charge interacting with a dummy variable equaling one beginning in 2009Q2 are each extremely statistically vital. They point out that the alternate charge elasticity over the 1994-2009 interval equaled −1.36 and over the 2009-2023 interval −1.36+1.05 = −0.31. Thus a ten% renminbi appreciation would scale back exports by 13.6% over the sooner pattern interval and by solely 3.1% over the later pattern interval.

Column (3) presents outcomes over the 1994-2009 interval. The alternate charge elasticity is accurately signed and higher than unity in absolute worth. Column (4) presents outcomes over the 2009-2023 interval. The alternate charge coefficient is now insignificant and near zero.

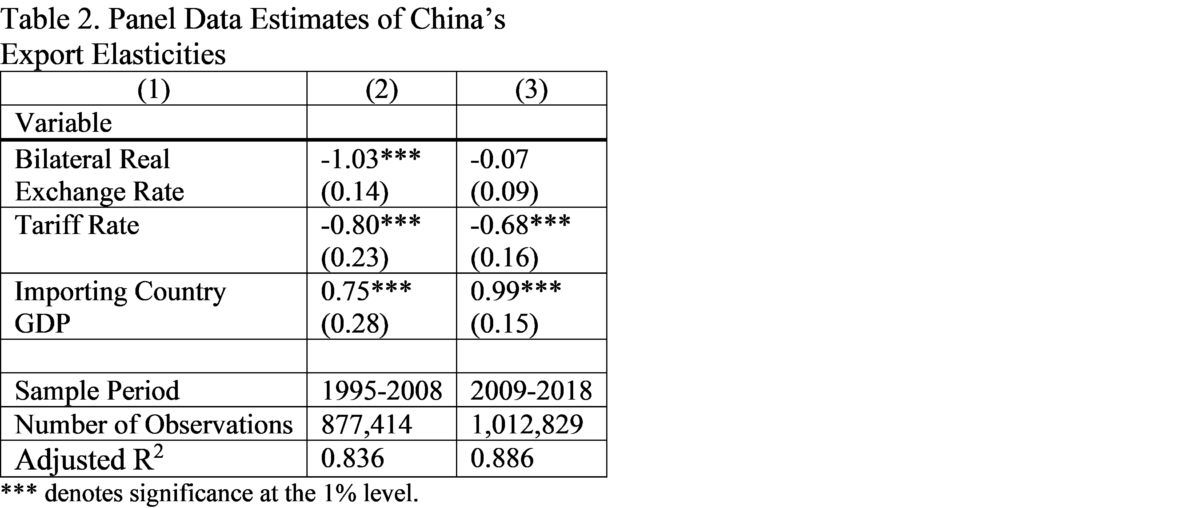

Panel Knowledge Proof on China’s Export Elasticities

One shortcoming of the strategy reported in Desk 1 is that we don’t management for tariffs. We are able to do that utilizing the methodology of Bénassy-Quéré et al. (2021). They defined annual disaggregated bilateral exports utilizing a collection of fastened results, the bilateral actual alternate charge between exporting and importing nations, the pure logarithm of 1 plus the bilateral tariff on a product, and different variables. We make use of information on China’s bilateral actual exports disaggregated on the Harmonized System four-digit degree for 1,242 export classes to 190 nations over the 1995 to 2018 interval.

Desk 2 presents the outcomes over the 1995-2008 and 2009-2018 durations. Column (2) presents the outcomes for the sooner pattern interval and column (3) for the later pattern interval. Within the precedent days the coefficient on the alternate charge elasticity equals −1.03. This means {that a} 10% renminbi appreciation would scale back exports by 10.3%. The coefficient on the tariff charge equals −0.80. This means {that a} 10 % improve in tariffs would scale back exports by 8 %.

Within the later interval the coefficient on the alternate charge equals −0.07. This suggests that the alternate charge doesn’t have an effect on Chinese language exports over the 2009-2018 interval. The coefficient on the tariff charge equals −0.68. This means {that a} 10 % improve in tariffs would scale back exports by 6.8 %.

We additionally examine whether or not alternate charges impacted extra subtle merchandise otherwise over the later interval, utilizing the tactic of Hidalgo and Hausmann (2009) to measure sophistication. We discover that alternate charges didn’t impression exports both for easy or for advanced merchandise.

Conclusion

China’s exports have soared. Setser (2024) reported that China’s items commerce steadiness could also be 50% larger than reported within the Chinese language present account information. China’s export juggernaut has generated tariffs overseas. Change charge appreciations is not going to assist to stabilize exports. Moderately than stoking protectionism, to rebalance commerce China ought to increase home consumption and nations just like the U.S. with outsized price range deficits ought to pursue fiscal consolidation.

References

Ahmed, S., Appendino, M., Ruta, M. 2015. World Worth Chains and the Change Fee Elasticity of Exports. IMF Working Paper No. 15–252, Worldwide Financial Fund, Washington DC.

Bénassy-Quéré, A., Bussière, M., Wibaux, P. 2021. Commerce and Foreign money Weapons. Overview of International Economics 29, 487-510.

Cheung, Y., Chinn, M., Qian, X. 2012. Are Chinese language Commerce Flows Completely different? Journal of Worldwide Cash and Finance 31, 2127-2146.

de Soyres, F., Frohm, E., Gunnella, V., Pavlova, E. 2021. Purchased, Bought and Purchased Once more: The Affect of Advanced Worth Chains on Export Elasticities. European Financial Overview 140, Article Quantity 103896.

Hidalgo, C., Hausmann, R. 2009. The Constructing Blocks of Financial Complexity. Proceedings of the Nationwide Academy of Sciences 106, 10570–10575.

Jean, S., Reshef, A., Santoni, G., Vicard, V. 2023. Dominance on World Markets: The China Conundrum CEPII Coverage Transient No 44, CEPII, Paris.

McMorrow, R. 2024. Huawei Laptop computer Reveals China’s Progress in the direction of Tech Self-sufficiency. Monetary Instances, 24 September.

Setser, B. 2024. The IMF’s Newest Exterior Sector Report Misses the Mark. Comply with the Cash Weblog, 26 August.

Xing, Y. 2021. Decoding China’s Export Miracle: A World Worth Chain Evaluation. World Scientific, Singapore.

This publish written by Willem Thorbecke.

{kind=link}