Right now, we current a visitor submit written by David Papell and Ruxandra Prodan-Boul, Professor of Economics on the College of Houston and Economics Lecturer at Stanford College.

The Federal Open Market Committee (FOMC) maintained the goal vary for the federal funds fee (FFR) at 5.25 – 5.5 p.c in its June 2024 assembly and, within the Abstract of Financial Projections (SEP), projected one ¼ p.c fee minimize with a variety for the FFR between 5.0 and 5.25 p.c by the tip of 2024. Futures markets summarized by the CME FedWatch Instrument after the assembly predicted two fee cuts with a variety for the FFR between 4.75 – 5.0 p.c by the tip of 2024. Evaluating prescriptions of inertial coverage guidelines the place the FOMC smooths fee will increase when inflation rises to projections from the SEP, the FOMC went from “on monitor” in March to “increased for longer” in June.

There’s widespread settlement that the Fed fell “behind the curve” by not elevating charges when inflation rose in 2021, forcing it to play “catch-up” in 2022. “Behind the curve,” nevertheless, is meaningless with out a measure of “on the curve.” In our paper, “Coverage Guidelines and Ahead Steerage Following the Covid-19 Recession,” we use knowledge from the SEP’s from September 2020 to December 2023 to check coverage rule prescriptions with precise and FOMC projections of the FFR. This offers a exact definition of “behind the curve” because the distinction between the FFR prescribed by the coverage rule and the precise or projected FFR. On this submit, we analyze 4 coverage guidelines which are related for the long run path of the FFR, replace the coverage rule prescriptions via the June 2024 SEP, and embody futures market predictions.

The Taylor (1993) rule with an unemployment hole is as follows,

the place is the extent of the short-term federal funds rate of interest prescribed by the rule, is the inflation fee, is the two p.c goal stage of inflation, is the 4 p.c fee of unemployment within the longer run, is the present unemployment fee, and is the ½ p.c impartial actual rate of interest from the present SEP.

Yellen (2012) analyzed the balanced strategy rule the place the coefficient on the inflation hole is 0.5 however the coefficient on the unemployment hole is raised to 2.0.

The balanced strategy rule acquired appreciable consideration following the Nice Recession and have become the usual coverage rule utilized by the Fed.

These guidelines are non-inertial as a result of the FFR totally adjusts each time the goal FFR modifications. This isn’t in accord with FOMC apply to clean fee will increase when inflation rises. We specify inertial variations of the foundations primarily based on Clarida, Gali, and Gertler (1999),

the place is the diploma of inertia and is the goal stage of the federal funds fee prescribed by Equations (1) and (2). We set as in Bernanke, Kiley, and Roberts (2019). equals the speed prescribed by the rule whether it is optimistic and 0 if the prescribed fee is adverse.

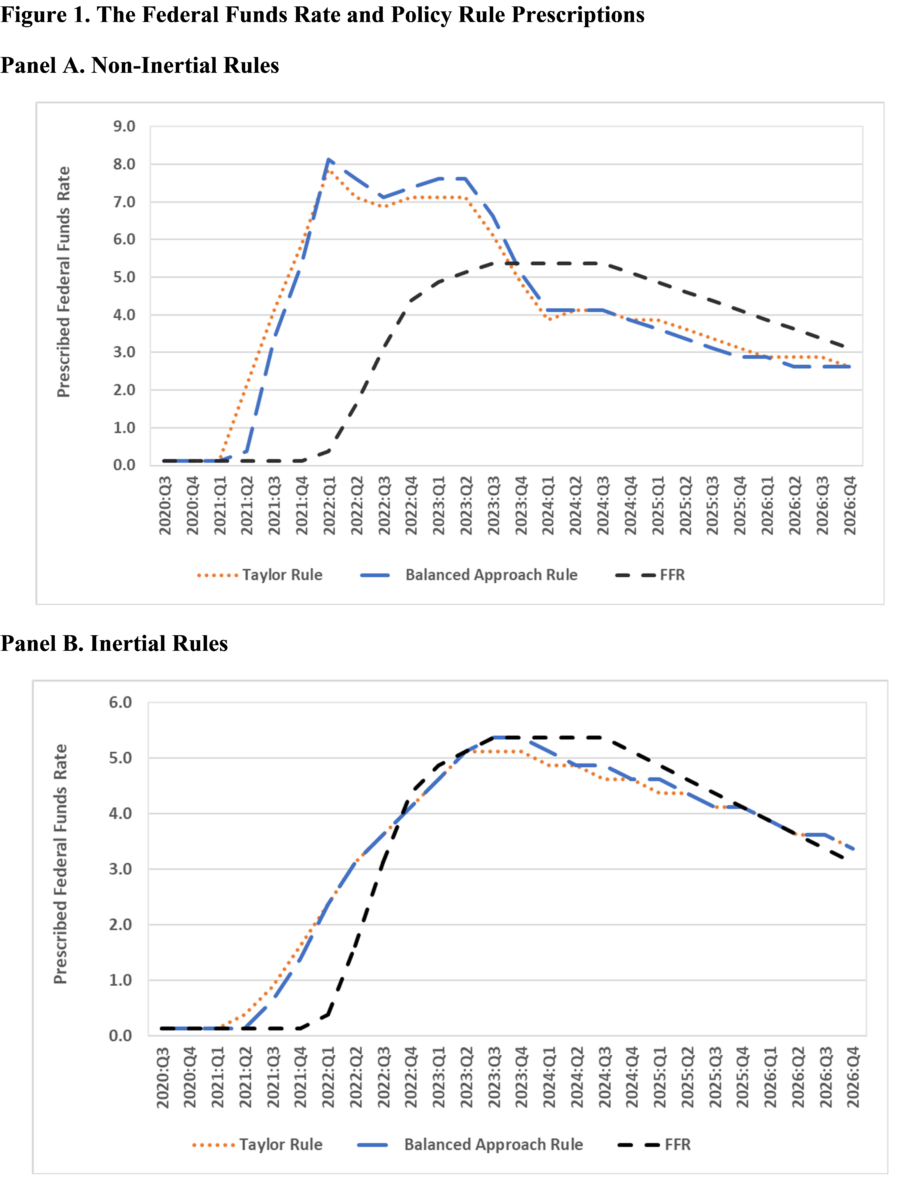

Determine 1 depicts the midpoint for the goal vary of the FFR for September 2020 to June 2024 and the projected FFR for September 2024 to December 2026 from the June 2024 SEP. Determine 1 additionally depicts coverage rule prescriptions. Between September 2020 and June 2024, we use real-time inflation and unemployment knowledge that was accessible on the time of the FOMC conferences. Between September 2024 and December 2026, we use inflation and unemployment projections from the June 2024 SEP. The variations within the prescribed FFR’s between the inertial and non-inertial guidelines are a lot bigger than these between the Taylor and balanced strategy guidelines.

Coverage rule prescriptions are reported in Panel A for the non-inertial Taylor and balanced strategy guidelines. They’re much increased than the FFR in 2022 and 2023 and aren’t in accord with the FOMC’s apply of smoothing fee will increase when inflation rises. In distinction, the coverage rule prescriptions for 2024 via 2026 from the June 2024 SEP are persistently decrease than the FFR projections. The inertial guidelines in Panel B prescribe a a lot smoother path of fee will increase from September 2021 via September 2023 than that adopted by the FOMC. If the Fed had adopted the inertial Taylor or balanced strategy rule as an alternative of the FOMC’s ahead steerage, it might have prevented the sample of falling behind the curve, pivot, and getting again on monitor that characterised Fed coverage throughout 2021 and 2022.

Trying ahead, the coverage rule prescriptions from the June 2024 SEP are under the FFR projections via September 2025 and are near the FFR projections via December 2026. Whereas the present and projected FFR is mostly in accord with prescriptions from inertial coverage guidelines, the gaps are bigger for 2024 than within the March SEP as a result of the FOMC projected three ¼ p.c fee cuts in March and one ¼ p.c fee minimize in June. The outcomes for the March 2024 SEP on this and the next two paragraphs are proven in our Econbrowser submit.

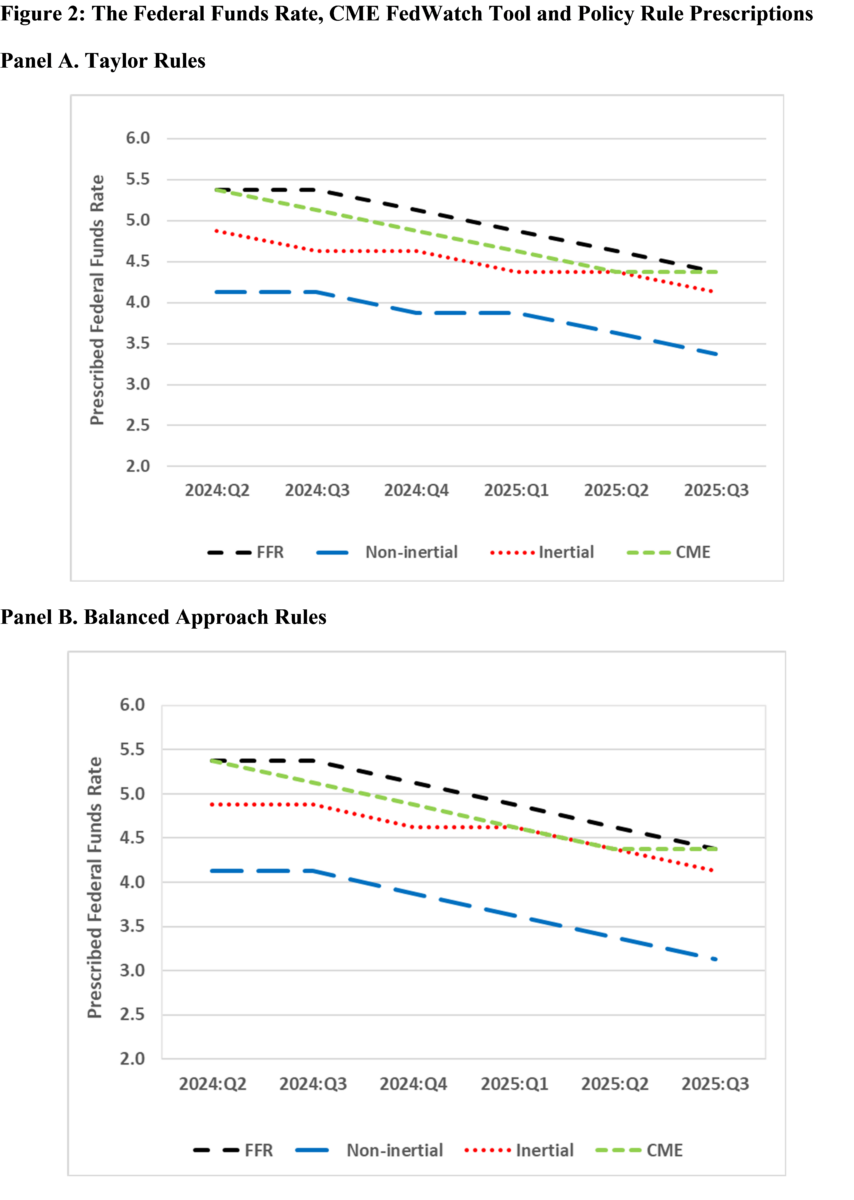

Determine 2 depicts the median predictions from futures markets described within the CME FedWatch Instrument following the June 2024 FOMC Assembly via the tip of the CME prediction horizon in September 2025. The futures market predictions are ¼ p.c under the FOMC projections earlier than converging on the finish as a result of futures markets predict two fee cuts whereas the FOMC tasks one fee minimize in 2014. The sample of decrease futures market predictions than FOMC projections is in line with December 2023 however not with March 2024, the place the predictions and projections had been equivalent.

We add to this dialogue by together with prescriptions from coverage guidelines. Determine 2 reveals that, for each the Taylor and balanced strategy guidelines, the prescriptions from the inertial coverage guidelines for June 2024 via December 2025 are typically under each the CME predictions and the FOMC projections however are nearer to the CME predictions than the FOMC projections. As well as, the hole between the inertial coverage rule prescriptions and the CME predictions widens between March and June of 2024. The prescriptions from each non-inertial coverage guidelines are significantly under the FOMC projections and CME predictions for a similar interval. Comparability between futures market predictions and coverage rule prescriptions relies upon extra on the selection between inertial and non-inertial guidelines than on the selection between Taylor and balanced strategy guidelines.

This submit written by David Papell and Ruxandra Prodan-Boul.

{kind=link}