I’ve solely gotten round to writing about this Trump coverage proposal: “Trump commerce advisers plot greenback devaluation” . I used to be befuddled by how they Trump mind belief was going to successfully drive the weakening of the greenback: sterilized intervention, dropping rates of interest within the US, or forcing overseas international locations to re-peg their currencies at stronger values. All of them appear to be problematic.

Sterilized intervention: There’s not a lot proof that for international locations with open capital markets this works, on an prolonged foundation (see Popper, 2022 for a survey).

Dropping US rates of interest: Nicely, if the US might drop rates of interest whereas forcing different international locations to lift their very own, this is able to (within the absence of no matter turmoil in monetary markets this would possibly trigger) depreciate the greenback. If as well as, by dropping US rates of interest one might persuade monetary market individuals that inflation would speed up, then most traditional financial fashions of the alternate charge would predict greenback depreciation within the brief run.

My estimates for an advert hoc mannequin 2005-2023 yields:

r = -5.61 + 2(y-y*) + 9.6i – 9.7i* – 0.81π + 1.51π* + 0.003VIX

Adj-R2 = 0.88, SER = 0.031, DW = 0.60, N =76. Coefficients in Daring point out significance on the 10% msl utilizing HAC strong normal errors.

The place r is log actual commerce weighted greenback, y is GDP, i is the ten yr yield, π is y/y CPI inflation, and * denotes rest-of-advanced economies. The match is proven in Determine 1:

Determine 1: Actual commerce weighted worth of US greenback (daring black), in-sample prediction (teal). NBER outlined peak-to-trough recession dates shaded grey. Supply: Federal Reserve by way of FRED, NBER, and writer’s calculations.

If this set of correlations holds up into the long run, then a one proportion level discount within the 10 yr Treasury yield relative to overseas would cut back the actual worth of the greenback practically 10 %. Is that this potential in apply? That is laborious to say; in spite of everything, long run charges are correlated, and different superior economies long run charges are inclined to comove.

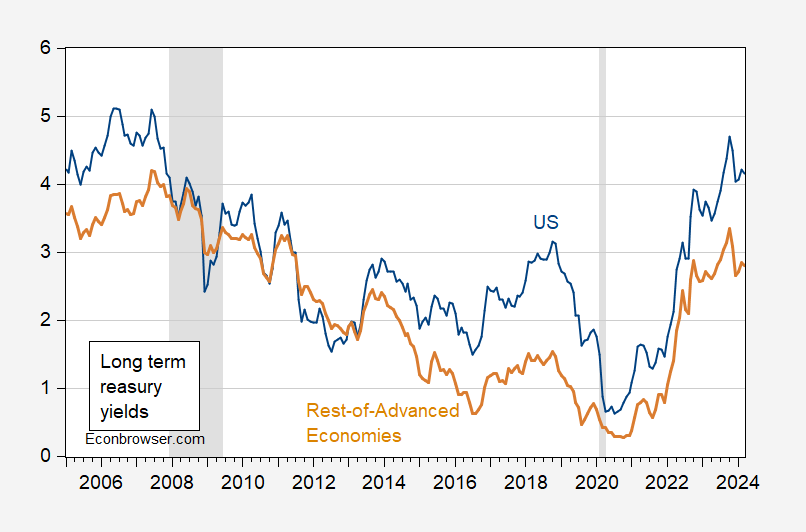

Determine 2: US Ten 12 months Treasury yield (blue), rest-of-advanced financial system long run (5-10 years) authorities bond yields (tan), each in %. NBER outlined peak-to-trough recession dates shaded grey. Supply: Treasury by way of FRED, Dallas Fed DGEI, and NBER.

On this pattern interval, each proportion level change within the US Treasury yield is related to a couple of 0.6 proportion level change within the rest-of-advanced financial system yields.

In fact, ought to charges be decreased within the US, then US GDP would doubtless develop quicker than in any other case, thereby barely offsetting the (already diminished) rate of interest impact. If the US has to exert some sturdy arm strategies to achieve the “cooperation” of different international locations, presumably the VIX would rise (because it typically did below Trump, notably throughout the commerce warfare). In fact, the US Treasury can’t in and of itself management the yield on Treasury bonds, in a market financial system. So the compliance of the Fed could be crucial (which may be why Trump’s mind belief is considering find out how to make the Fed decision-making course of extra malleable).

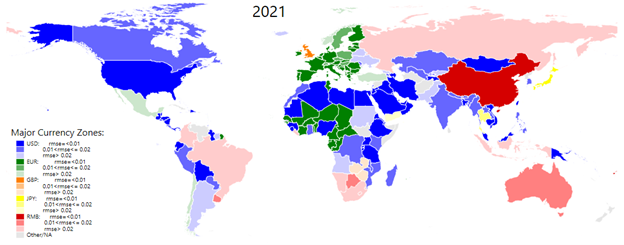

Forcing different international locations to revalue: The nominal worth of the US greenback is a operate of insurance policies within the international locations pegging to the greenback. Ito and Kawai establish foreign money zones as these pegging to respective currencies. As of 2021:

Determine 3: The Evolution of the Main Forex Zones. Supply: Compiled by authors from their estimations. Supply: Ito (2024).

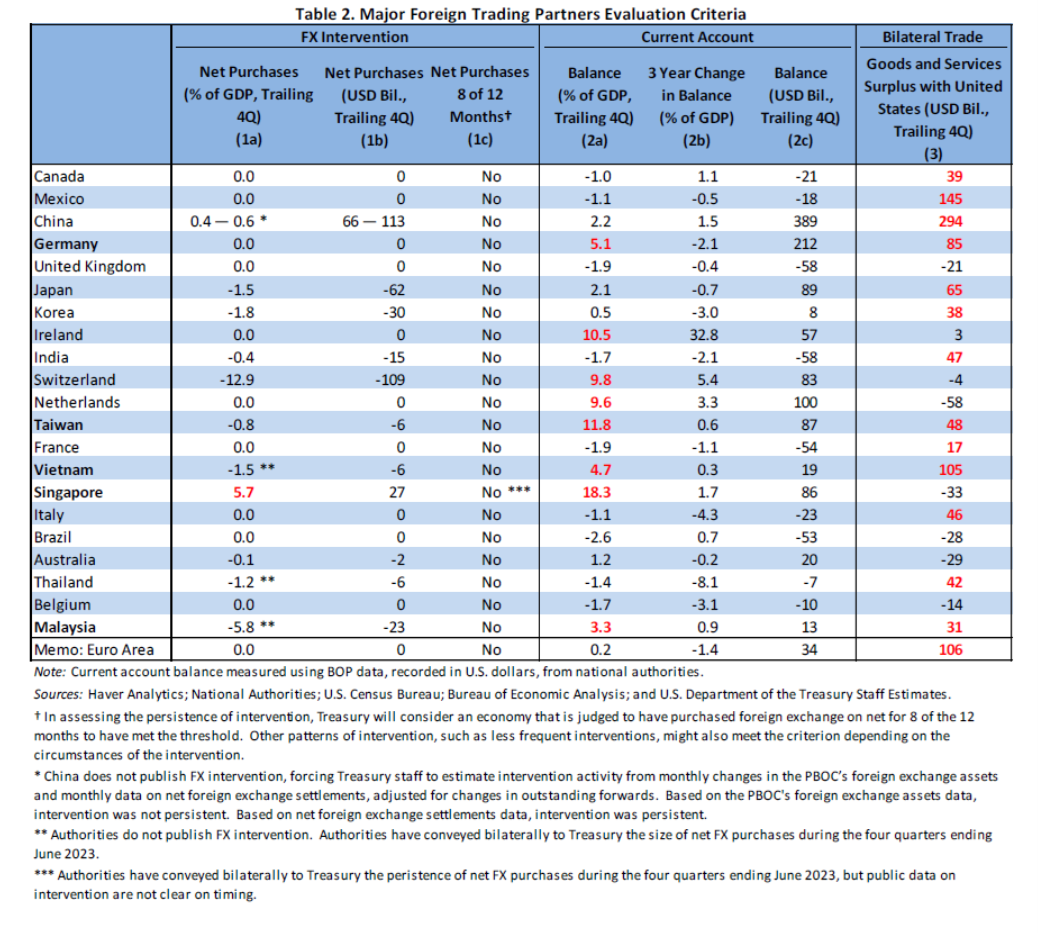

Of these international locations recognized as being within the greenback zone, not all peg, or quasi-peg, to the greenback. However people who do, the US might cajole into revaluing. How large of an impact? Adler, Lisack and Mano (Rising Markets Evaluate, 2022) discover that every one proportion level of GDP discount in FX intervention appreciates a bilateral actual alternate charge by between 1.4-1.7 ppts. There may be some query whether or not China has returned to a greenback peg as of 2024, however we will look at how possible it’s to get a giant appreciation of the US greenback by analyzing how a lot intervention is occurring now. The final US Treasury FX report, in November 2023, presents some statistics.

Supply: US Treasury (November 2023).

Singapore is intervening considerably (as a share of GDP), however has solely a 1.9% weight within the commerce weighted greenback (broad US Fed). China has a much bigger weight, 13.4% [1]. If China had been to scale back intervention by 1 ppt of GDP (the place it was estimated at 0.4-0.6 ppts by Treasury), then the RMB would admire by 1.4-1.7%. The direct influence on the commerce weighted greenback would then be 0.23 ppts to 0.28 ppts(!). To the extent that some international locations peg their foreign money to the yuan, then one would possibly get a barely greater impact. Nonetheless, ultimately, it looks as if a number of work to get a small change within the worth of the greenback.

Extra analysis of the desirability of this coverage initiative, by Rampell (WaPo), in addition to Horan (Nationwide Evaluate).

{kind=link}