Yves right here. Even earlier than Trump’s price-goosing tariffs are prone to coming into play, key inflation metrics are going the flawed approach.

By Wolf Richter, editor at Wolf Road. Initially printed at Wolf Road

Inflation has been in providers and remains to be in providers, it has develop into sticky in providers, and lately it has been re-accelerating in providers. Companies dominate client spending. And sturdy items costs rose for the second month in a row, after huge drops. However gasoline costs continued to plunge, and meals costs ticked up just a bit, in keeping with the PCE worth index by the Bureau of Financial Evaluation at present. That is the info the Fed prioritizes as yardstick for its 2% inflation goal.

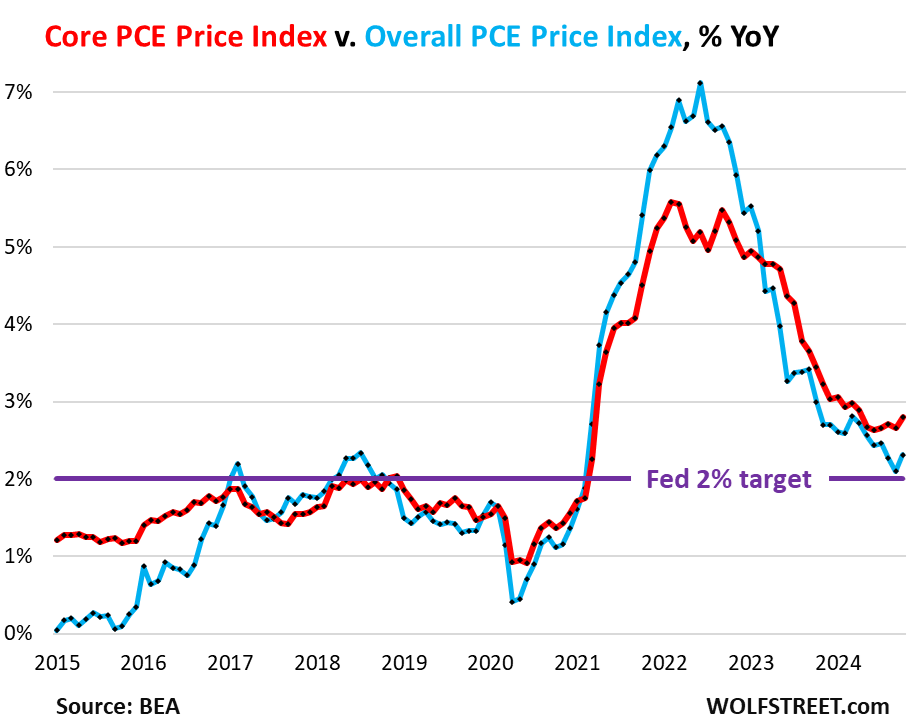

Three of the 4 main metrics accelerated in October even on a year-over-year foundation: the general PCE worth index to +2.3% (blue), the “Core” PCE worth index to +2.8%, (purple), and the “Core Companies” PCE worth index to +3.9% (gold), whereas the sturdy items PCE Value index began rising from the ashes and have become much less unfavorable (inexperienced).

The Fed has already been speaking down the tempo of future fee cuts lately, together with within the assembly minutes yesterday and in speeches by Fed governors.

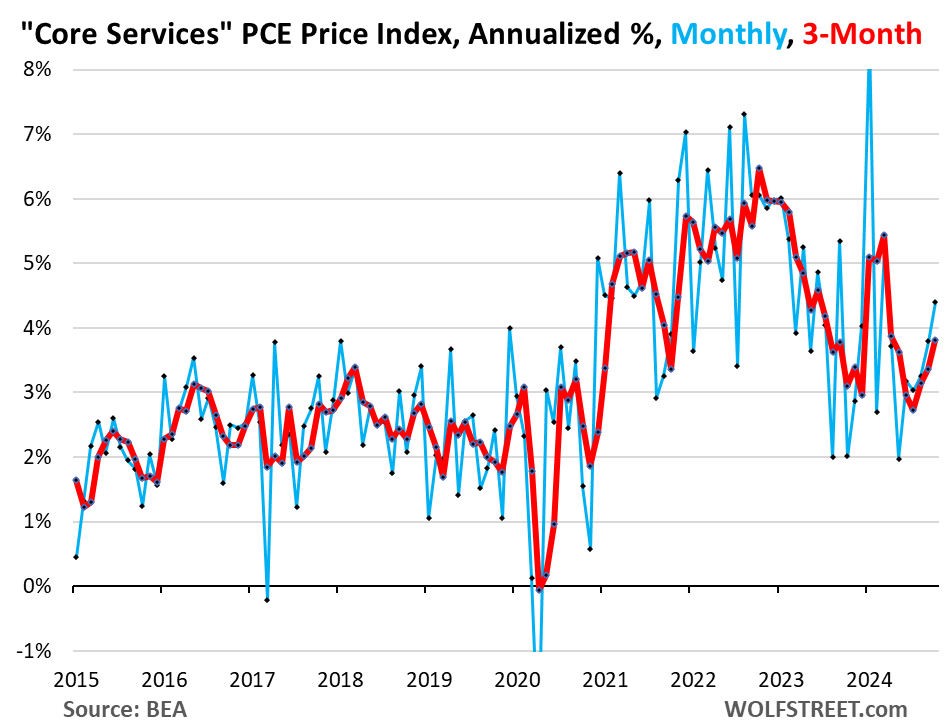

The driving force: “Core Companies.” The PCE worth index for “core Companies” accelerated to +4.4% annualized in October from September (+0.36% not annualized), the sharpest improve since March (blue within the chart beneath). The three-month core providers index accelerated to three.8% annualized (purple).

Core providers embody housing, healthcare, monetary providers & insurance coverage, transportation providers, non-energy utilities, communication providers, recreation providers, meals providers & lodging, and “different” providers. Nevertheless it excludes vitality providers, resembling electrical energy to the house.

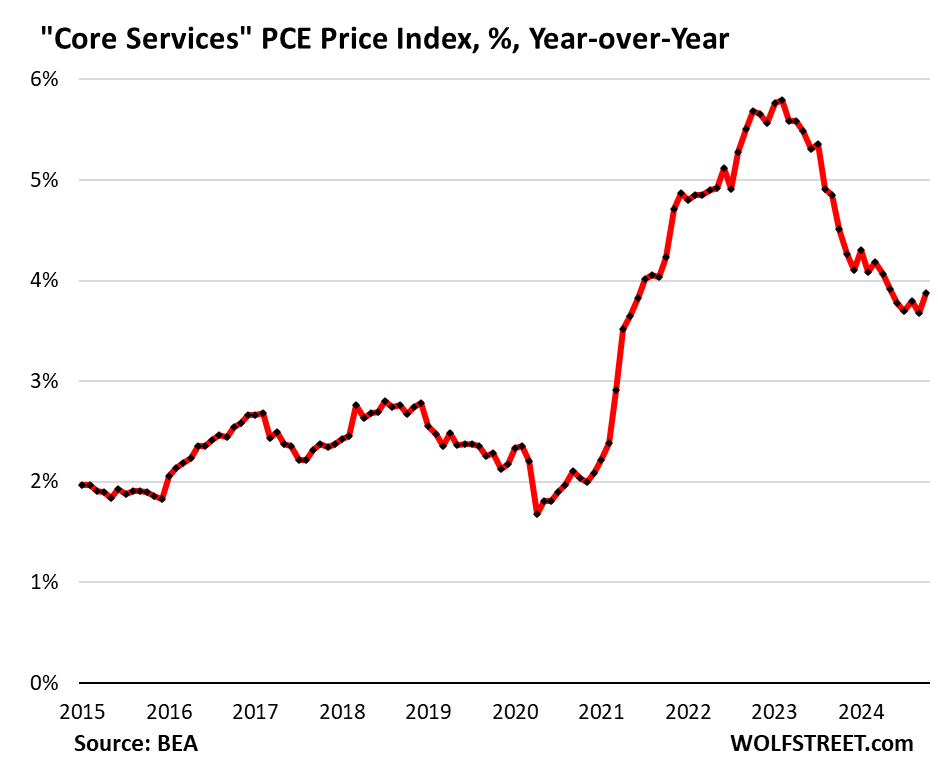

12 months-over-year, core providers PCE worth index accelerated to three.9%, the quickest improve since Could. There has basically been no progress since Could:

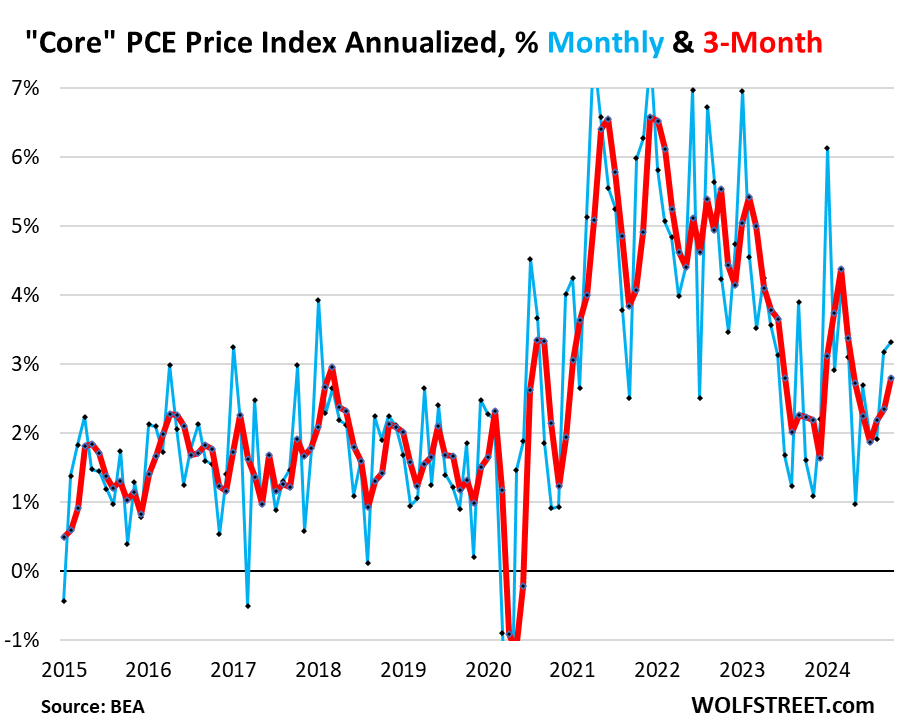

The “core” PCE worth index accelerated to +3.3% annualized in October from September (+0.27% not annualized), the most important month-to-month improve since March.

This month-to-month acceleration was pushed by the bounce within the core providers PCE worth index (see above).

The “core” index makes an attempt to point out underlying inflation by excluding the parts of meals and vitality as they will bounce and drop with commodity costs.

The three-month core PCE worth index accelerated to +2.80% annualized, the third acceleration in a row, and the quickest improve since April (purple).

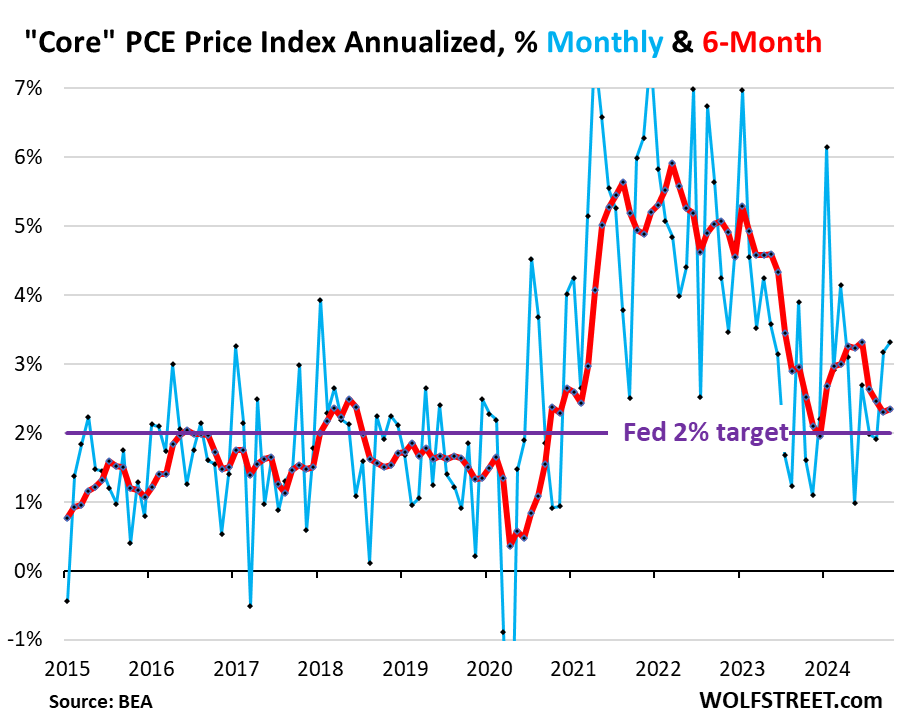

The 6-month core PCE worth index accelerated to +2.34% annualized (purple), and has remained greater all 12 months than it had been on the finish of final 12 months:

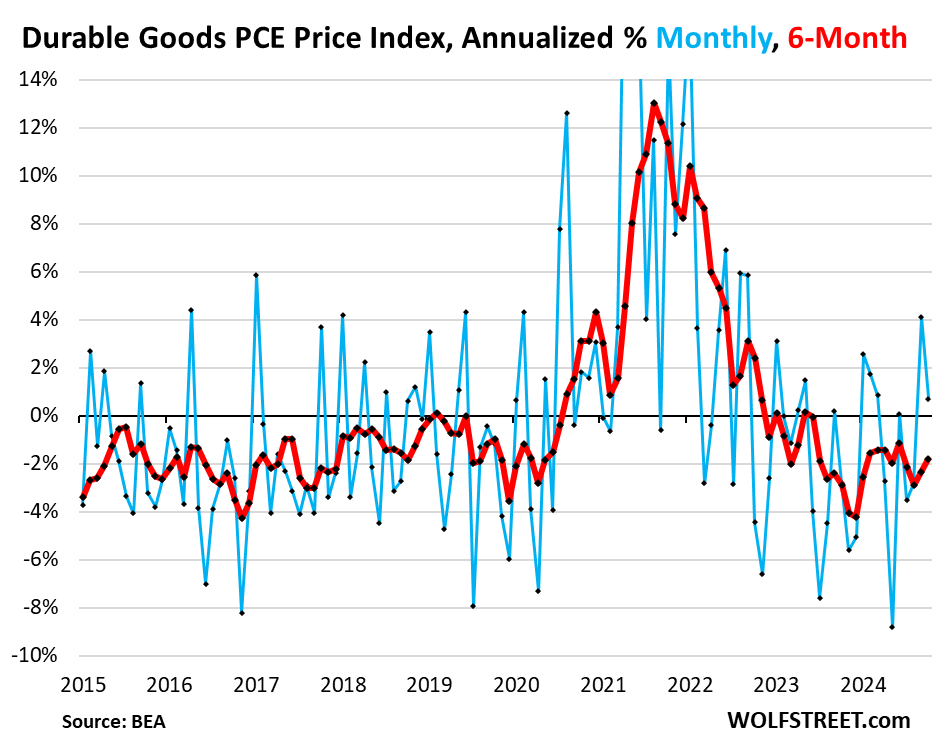

The sturdy items PCE worth index elevated by 0.7% annualized (+0.06% not annualized) in October from September, on prime of the large bounce in August, which had been the most important improve in two years, after a sequence of steep unfavorable readings (deflation).

In October, the month-to-month improve was as a consequence of motor automobiles, whereas costs fell for family furnishings & home equipment, leisure items & automobiles, and “different” sturdy items.

In consequence, the 6-month index turned much less unfavorable (-1.8%, purple line).

And the year-over-year index additionally turned much less unfavorable, see inexperienced line in first chart on the prime (-1.6%).

In latest a long time, sturdy items costs trended decrease on common as a consequence of manufacturing efficiencies, technological enhancements, and offshoring manufacturing to low-cost nations (globalization). Over these a long time, the driving pressure in inflation has been providers. Throughout the pandemic, sturdy items costs spiked as a result of sudden demand fueled by huge financial stimulus that made customers out of the blue keen to pay no matter for items, and there was large demand for items, overwhelming provide chains, giving corporations monumental pricing energy, they usually used that pricing energy:

The general PCE worth index, which incorporates the meals and vitality parts, rose by 2.3% year-over-year in October, an acceleration from September (+2.1%), regardless of the plunge in gasoline and different vitality costs of -12.4% year-over-year and -1.0% month-to-month (not annualized).

Meals and vitality costs make up the distinction between the general PCE worth index (blue) and the core PCE Value index (purple). The worth spikes of meals and vitality in 2021-2022 brought about the general PCE Value index to shoot to +7%, whereas the core PCE worth index, which tracks the underlying inflation past commodities costs, topped out at 5.5%.

As vitality costs have been plunging beginning in mid-2022, the general PCE worth index decelerated sooner than the core PCE Value index, leaving the core PCE worth index with a better fee.

{kind=link}