With December 31 information, right here’s the image of time period spreads:

Determine 1: 10yr-3mo Treasury unfold (blue), 10yr-2yr Treasury unfold (crimson), each in %. Supply: Federal Reserve by way of FRED, creator’s calculations.

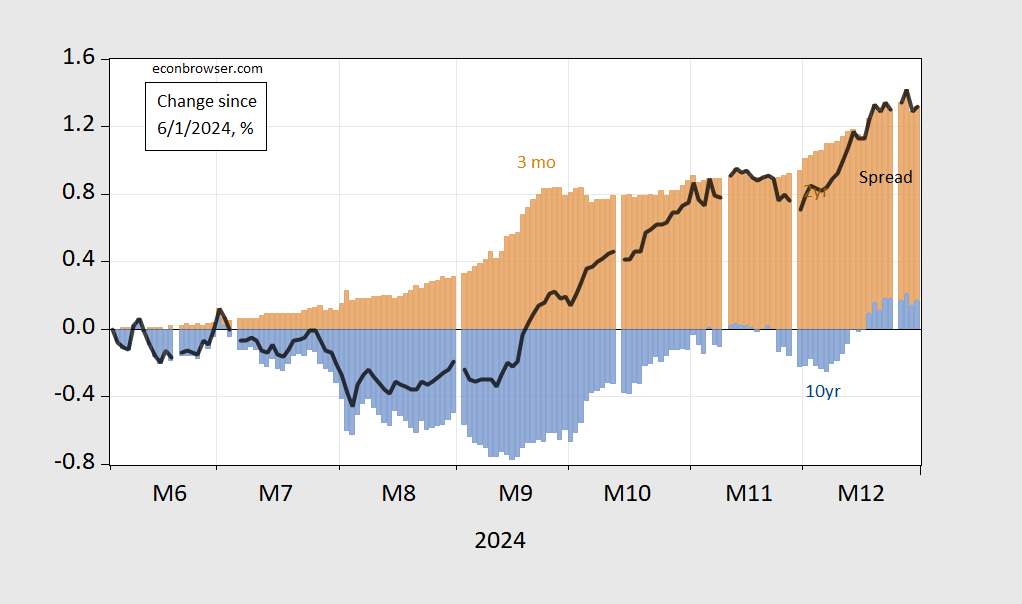

Bull or bear steepening within the 10yr-3mo? Right here’s each day information:

Determine 2: Change since June 1, 2024 in 10yr-3mo time period unfold (daring black), contribution to alter from 10 12 months yield (blue bars), from 3 month yield (tan), all in proportion factors. Supply: Treasury by way of FRED, and creator’s calculations.

It’s the case that almost all of the disinversion since June 1st is as a result of quick fee falling, not the lengthy fee rising.

Utilizing a specification incorporating the three month change within the unfold, a probit mannequin implies 61% likelihood of recession in 2025M04, in comparison with 31% utilizing a selection solely…

{kind=link}